A small reflection exercise to start with:

just think of someone you consider professionally and financially successful. Got that person visualized? Now, is that person renting or owning their house?

The answer to that question kind of summarizes the most important difference between renting and buying a property, in Spain or anywhere in the world: when owning you create wealth for yourself, when renting you help your landlord getting wealthier. Of course, renting can be an easier and better option in the short run, it gives you more flexibility and requires less commitment. But in this article, I go beyond the textbook comparison. I will give you a deep dive analysis of why owning a property is (often) the better solution, with practical exercises to compare both options in your specific situation and with your actual income and savings. So in the end, you also know what type of property you can afford at which cost per month.

Now is the good time to switch from your renting contract to one at the notary.

Create Wealth for You or for Your Landlord?

The choice between renting or owning comes down to the question above. I’ll give you an overview of the pros and cons of both options.

Renting

- Renting gives you the certainty of using an apartment till the end of the month (or end of a contract), but you get no real personal asset in the long term.

- Doesn’t allow you to create leverage on your savings. If you have a certain amount of savings, a rental agreement will not create any opportunity to increase those savings.

- Reduces your ability to save money.

- Can be a good temporary solution, with less commitment and more flexibility.

Owning Your Property

- Buying a property creates wealth for you and your family. Owning a property could be a first step to financial independence. Once the house or apartment is yours, you can potentially rent it out, or sell it at a profit. You can even call it a potential pension plan.

- Buying often upgrades your living situation. It’s very common for people to buy a property that is better than the one they previously rented. They often know more about which area they want to live in, which housing features they want and don’t want, and they are more eager to decorate and change the lay-out to their needs than in a rented property owned by someone else.

Renting or Buying a Property? Comparing the Options with Actual Numbers.

Let’s go beyond the theory and compare both options with an exercise that contains your actual numbers and financial indicators—probably in a way you never looked at before.

The table below shows different monthly rental amounts as the starting point. Let’s visualize it with a different persona: You’re new in Spain and start off by renting a room in a shared apartment for €500 per month. This is a classic starting situation in cities like Barcelona. That will cost you €6,000 per year or €60,000 over 10 years. Why 10 years? That is the average period people generally rent. That might sound long, but 10 years go by faster than you think.

You might get older and get the desire for a place of your own, then €1,000 rent per month can be a perfect average number. That’s €120,000 for your landlord in a period of 10 years.

The table gives a number of other rental amounts, but let’s say if you are between 40 to 50 years old, you might prefer another type of property (a penthouse, a more upscale location) and pay around €1,600 per month, or up to €200,000 rental cost over a period of 10 years.

Discover your own situation in the table below (taking into account these illustrations are not adapted for inflation or any other economic or financial impact):

Now compare this rental cost to your financial situation. Again, a table with different options.

Imagine your net income is €2,500 per month, or €30,000 per year net (that will be around 50,000 to 60,000 gross). If your monthly rental cost is then €1,000 and you rent for 10 years, that means you need to work four full years to pay that rent. That’s nearly two weeks per month you work for your landlord.

Of course, if you earn more, that number will decrease. If your net income is €5,000 per month, and you’re still in that €1,000 flat, then it takes you only two years to pay off your 10 year rent.

What Can I Do With My Savings?

In the rent-or-buy dilemma, the decision to actually start the buying process often depends on the amount you have saved. That also came to surface during a recent market research analysis at INSPIRE. When asking potential customers the simple question “Why didn’t you buy yet?” the top answer was “not enough savings.”

But let’s go a step back and look at what alternatives you have for your savings, and why it’s more interesting to put it into a house or a mortgage down payment.

Imagine you have €60,000 in savings. What can you do with that?

- Rent a property of €1,000 per month for five years. As mentioned before, this option is good for the landlord but has no future value for you, as you’re not creating wealth for yourself.

- Keep it in your bank account. This traditional option means liquidity and easy access to your money, but in the long term your value will decrease year after year as banks are starting to charge fees to hold your money.

- Invest in the stock market or investment funds. This decision is more volatile, which means you have more potential to gain, but also more to lose. So, if you worked hard for your €60,000 savings, what risk do you want to take in losing it?

- Use it to buy a property. Leverage your €60,000 savings with a mortgage to own a house of €150,000 to €300,000 or even up to €400,000.

Let’s dig into this last option a bit more.

How Much Property Can I Buy with My Savings?

In my daily job as a property buyer agent in Spain, the number one remark I always get from buyers is: “I don’t know what I can actually purchase.” Or sometimes it’s phrased as: “I’m not sure what I want exists,” or “I don’t know if the bank will give me enough money to purchase what I want.”

In that previous example of €60,000 savings, I revealed the outcome already without much further explanation: give those €60,000 to the bank with a mortgage that gives you access to a house worth up to €400,000.

That is called “financial leverage”: you buy a property with limited savings and you can get access to something that is worth X times that investment. As the house will be yours, it can provide you with future rental income that exceeds the costs of the mortgage and other owner-related costs. It becomes a long term asset that can increase in value and generate future income/capital gains. That is called the “multiplier effect.”

For all those other investment options, the stock market for example, that leverage effect does not exist. Your €60,000 investment will be worth nothing more than that €60,000 (at the start).

How much money a bank decides to give you, taking into account your savings and your specific property and situation, depends on their loan to value ratio (LTV). And, of course, also assuming you have a stable income, a work contract and a normal spending profile.

If you are a Spanish resident (paying taxes in Spain) with a classic standard-risk profile, that LTV% typically goes up to 80% or in some cases even to 90%. That means you only need to put 20% or 10% of your own savings on the table. That percentage drops if for example, you’re not a resident or are independent. But it’s always worth talking to different banks to get their appraisals. Every bank is different and looks differently at your profile. Some banks prefer first time buyers (to get them for a longer lifetime), other banks are more risk-averse and prefer people with more money in the bank.

So How Much Money Do You Need to Put On the Table and How Do Banks Look at That?

Let’s explain it with an example, in the table below.

Two scenarios:

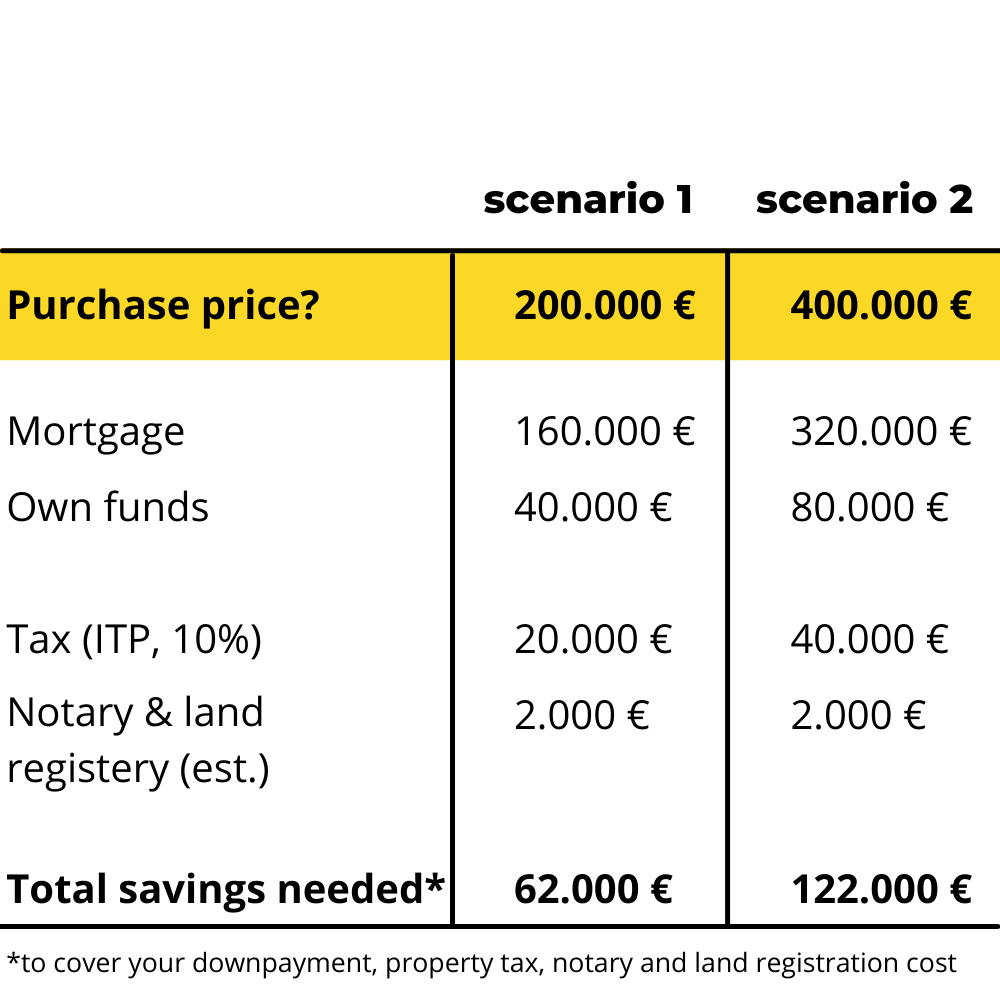

Table 1. The bank is NOT financing the purchase tax (of 10%)

Here, I took two options for the property purchase price: €200,000 and €400,000. If the LTV% is 80% and you need to put a 20% down payment, that is €40,000 or €80,000. And then your mortgage needs to be €160,000 or €320,000.

Some additional costs apply to purchasing a property in Spain:

The purchase tax (10% of the purchase price) and some notary and land registry costs (in total no more than around €2,000). As stated, in this scenario, the bank does not finance these costs, so you’ll need to pay them out of your own pocket.

Adding that means:

- with €62,000 savings you can buy a €200,000 house.

- with €122,000 savings you can buy a €400,000 house.

Table 2. The bank is financing the purchase tax.

This was an actual INSPIRE customer case a couple of months ago. So if the bank is offering you a higher LTV% (in this case 87%) and they also finance the taxes and extra costs, then you can buy a property of €400,000 with only €59,000 in savings.

Of course, not every bank does that. And your monthly payment will be different in the two scenarios too.

Your next step should then be: how much can you afford to pay to the bank each month? What amount of cash-out fits your lifestyle?

Concrete Example of a Recent Buyer

Let me share with you another practical, real-life example of a recent client of INSPIRE. Let’s call him Mike. Mike had around €50,000 in savings and was renting a room in a shared apartment in Eixample, Barcelona. He paid €550 per month for the room.

He was tired of sharing his home, wanted more privacy and peace and asked us to help him find a place of his own. And we did. We found him a move-in ready, three-bedroom, 63 square meter apartment, with some outside space. It’s located in Vallcarca, so a bit outside the city center of Barcelona, but it’s quiet, with lots of parks and it’s still very well connected to the center. It’s an area he adores.

We negotiated the purchase price down to €220,000, while the bank valued the property at €230,000. His down payment to the bank was €44,000 (20%) and because he met some specific criteria of age and income, he benefited from a reduced 5% purchase tax. With a 1.4% fixed interest rate over 30 years, he now pays €600 per month for his mortgage.

The big picture is clear: with a similar budget, Mike now has his privacy, and a bigger apartment than the room he was living in before.

But financially, is Mike really better off? As he is paying €600 per month now to the bank, instead of €500 to his landlord, he’s paying €50 more monthly. But, comparing payouts is not really the correct way. The true new housing cost for Mike is not the total mortgage payment, but the interest rate alone, as this is the true cost of his mortgage.

Breaking down the €600 monthly cash-out: (year one)

- Principal and capital (at start): €400

- Cost in interest (at start): €200

This €200 interest cost needs to be compared to the rent of €550. So, long term, Mike has a monthly savings of €350! Additionally, Mike now owns his apartment, so he gets something in exchange for the monthly cost that previously went to his landlord.

Cost of Buying a Property in Spain

Besides the cost of a mortgage, owning a property in Spain comes with some other costs as well. Let me give you an overview, connected with an example of a €300,000 property.

One-off Costs

- Purchase price: of course, that €300,000 property price needs to be paid either with cash or a mortgage.

- Purchase tax: 10%, or 5% when you meet certain age restrictions and income criteria (for young buyers).

- Notary and land registry costs: typically around €2,000.

Annual Costs

- City taxes. This amount depends on the village or city you live in, and in cities like Barcelona, the costs can vary depending on the street and size of your property.

- Home insurance.

- Community costs (only for apartments) include standard costs of maintenance of the building, cleaning the common areas, insurance for the building, maintenance of the elevator and roof, etc. The cost varies, and depends on the building’s prestige.

Variable Costs, Connected to a Mortgage

- Interest rate.

- Life insurance—your bank might require you to take a life insurance together with your mortgage.

Others Costs, If Applicable

- Renovations, maintenance and repairs. A bank typically does not finance a renovation, so you need to cover that cost.

- Buyer agent—this is a cost that can be of negligible value if you don’t want to end up with much bigger costs related to technical failures or legal issues.

In General, the First Step in Your Rent-or-Buy Decision (Or Any Property Purchase) Should Be:

- Do NOT start by looking for properties; first check what is financially possible.

- Talk to different banks, ask for simulations with different interest rates and evaluate the monthly mortgage costs.

- Ask for pre-approved mortgage offers, because it’s a bank’s strategy to tell you a simulation or verbal agreement will be OK by the time you have found a house. That will make you less eager to ask for offers from other banks afterwards. When the moment arrives and you have found a property, your bank might take advantage of the fact you need to react quickly with no time to negotiate a higher offer or go to another bank.

Having these financial numbers in mind, you should always be mindful of the fact that owning a property puts you in a better financial position; it makes your money productive by investing in something that is yours. So, analysis your situation well and if buying turns out to be your perfect solution; maybe you’ll turn out to be the “professionally and financially successful person” you thought of in the beginning of this article.

Stay an Informed Player

If you want to be well-versed, save money, avoid disturbances and conflicts of interest, this is what you can do:

* Join our Real Estate Series with 2-monthly webinars offering no-nonsense insights and tips to make better decisions and avoid mistakes. Check the top of this blog page for the lastest info & links to register for the next episodes, all for free.

* Contact me to discuss your plans and receive my recommendations (first consultation is free): raf@inspireapartments.com.